Signs You’re Doing Well Financially: 8 Key Personal Finance Ratios and Metrics You Need to Know

Have you ever wondered if you're truly on track financially? Maybe you budget and save, but still question if it's enough. As a financial coach, I hear this often. Many people seek the reassurance of knowing they're making the right financial moves. But the truth is, it can be hard to tell because everyone’s situation is different and there are many ways to measure success.

That’s why it is often helpful to analyze your finances by looking at certain personal finance ratios and metrics. These serve as signs that you’re doing okay financially, but they can also be used to determine underlying causes of financial stress.

These indicators help you diagnose problems, make informed decisions, and adjust your finances to achieve your goals.

Keep in mind that these numbers are guidelines and should not be used to determine if your finances are good or bad. The important thing is to measure them against yourself so that you can see progress over time. There are naturally certain times and situations where they will simply be lower, and that might be okay.

When I look at these numbers with my clients, it’s not to score them like a report card—they simply serve as a starting point to help us understand what is happening with their finances, what might be going wrong, and to identify ways to make things better.

I know these terms can seem intimidating. It's normal to feel overwhelmed, but don’t let that deter you. I'll break down each ratio in simple terms so you can confidently apply them to your finances. And if it still feels overwhelming, we can work together to use these metrics to build wealth and reduce stress.

In this article, we'll explore eight key personal finance ratios and metrics that reveal if you're doing well financially. By understanding and monitoring these figures, you'll gain clarity on your financial situation and be better equipped to make strategic improvements. Let’s dive in and uncover the signs that you're on a path to financial success.

8 Key Personal Finance Ratios and Metrics

1. Net Worth

When we think of net worth, many of us conjure mental images of wealthy individuals like Warren Buffet or Jeff Bezos. That’s because the term “net worth” is often associated with high net worth individuals—people who have a LOT of money. But calculating your net worth is something everyone should do to track their financial progress over time.

What is net worth?

Net worth is your assets minus your liabilities. In other words, it’s what you own minus what you owe.

Your assets include all the money in your accounts plus the value of the things that you own. So it includes your bank accounts, the current value of your investment and retirement accounts, and the value of tangible items like your home or car if you were to sell them today.

Your liabilities are the total of your outstanding debts and unpaid bills—anything that you owe to other people or companies.

What does your net worth tell you?

Your net worth has nothing to do with your self-worth and should not be used as a point of comparison to others. Nor should the number itself cause you to feel bad about yourself. It is normal to have a lower (or even negative) net worth when you are younger. Everyone starts somewhere.

Instead of focusing on the number itself, you should focus on making progress—on increasing the number. Your primary goal in tracking your net worth is to ensure that you are improving your financial position by increasing your assets and/or reducing your debt.

Net Worth Goal: Increasing the number over time

2. Net Cash Flow

Net cash flow is a term often used in the business world, but it’s important for individuals and households to calculate it as well. It tells you if you are spending more or less than you earn.

What is net cash flow?

To calculate your net cash flow, add up all the money you have coming in and subtract the money going out. In other words, it is income minus expenses.

Income includes any money earned from work (salary, wages, tips) as well as other payments you receive, such as:

Bonuses and commissions

Social Security income

RMDs (required minimum distributions from retirement accounts)

Investment income that is not reinvested

Tax refunds

Rental income

Royalties

Child support and alimony

SNAP benefits

Housing allowance

Scholarships and grants paid to you

Expenses include all money going out of your accounts, such as:

Regular bills (housing, utilities, insurance, day care, internet, etc.)

Money transferred to long-term savings

Debt payments (mortgage, car loans, student loans, payments on past-due credit cards)

Living expenses (groceries, medical bills, household supplies, personal care, home maintenance, gas)

Everything else (fun, entertainment, eating out, vacations, etc.)

Although money put into savings is not technically an expense, it’s a good idea to list it as one to ensure it remains a priority. You want to make sure you have enough income to save money, pay your bills, and buy the things you want and need.

Use your actual spending numbers instead of what you think or hope you are spending. Many people avoid doing this because it can be hard to face the reality of their spending. But it is a necessary step in taking control of your finances and reducing money stress.

If you struggle with this, a financial coach can help you figure out what to do and provide emotional support and accountability so you can move forward and ultimately feel better about your finances.

What does your net cash flow tell you?

Your net cash flow number indicates if you are spending more or less than you are earning. If your net cash flow is negative, it means you are accumulating debt. If your net cash flow is positive, you have money left over each month and could afford to save more or spend on things you enjoy.

Net Cash Flow Goal

Ensure this number is not negative. It’s okay for this number to be zero as long as you are also saving enough money (see savings rate below).

Note: If you have a positive cash flow but still struggle to pay bills, you may have a timing problem. For example, if you are paid every two weeks or twice per month but your bills are all due at the beginning of the month, you might not have enough money to pay them on time. This is something a financial coach can help you figure out.

3. Fixed Cost Ratio

Your fixed cost ratio essentially measures how much flexibility you have with your finances. Is all of your income tied up in necessary expenses, or do you have enough flexibility in your budget to buy things you want and need when it makes sense to do so?

What is the fixed cost ratio?

The fixed cost ratio is found by adding up everything you need to survive and avoid significant consequences and dividing that number by your total net income. Let’s simplify and explain:

Fixed Costs

Fixed costs are the things that you have to pay. In other words, they are your needs. If you didn’t pay for them, you would suffer major consequences, such as losing your home or car, not eating, being unable to work, having health problems, or losing access to electricity or water.

To calculate your fixed costs, find the average amount you spend each month on:

Housing

Utilities (Gas, electricity, water, trash/recycling, phone/internet)

Transportation (Auto loans, gas, regular maintenance, public transportation)

Insurance (Home/renters, auto, anything not deducted from your pay)

Taxes not deducted from your pay

Groceries

Clothing and personal care items that you need

Medical costs

Child care

Debt payments

Child support/alimony

Home maintenance

Anything else that would cause significant hardship if you didn’t pay for it

Remember to include the average monthly amount for anything not paid monthly, such as insurance, property taxes, car tabs, and yearly memberships.

If you’re unsure if something should be included in fixed costs, ask yourself what would happen if you didn’t buy it. Would it mean you aren’t able to live your life, or would it mean missing out on leisure activities like watching your favorite show, golfing, or eating out?

It’s important to have money to spend on things you enjoy. One reason to calculate your fixed cost ratio is to ensure you have enough money for these things. You want to keep your fixed costs (needs) low enough that you can spend money on things you want and that make your life better.

Once you have your total average monthly fixed costs, divide it by your monthly take-home pay. This is the amount you are paid after taxes, retirement contributions, health insurance costs, and other deductions are removed. It’s the amount that lands in your checking account.

Fixed Cost Ratio: Total fixed costs divided by total take-home pay

What does your fixed cost ratio tell you?

Your fixed cost ratio tells you how much of your available income is tied up in things you have to pay.

Having a high fixed cost ratio means that your bills and necessary living expenses are so high that you struggle to save money and have little left for flexible spending on fun and things you want. Conversely, having a low fixed cost ratio means you have a lot of disposable income after paying for what you need.

Paying attention to this number helps you understand how stressful your financial situation is likely to be and if you have enough money to save for the future and enjoy life now. When your fixed costs are high, it increases the likelihood that you feel stressed about your finances, struggle to save money, may have to rely on debt, and don’t have enough to spend on things you love.

Fixed Cost Ratio Goal

Aim for this number to be 50-60%.

If your fixed costs are above 60%, identify ways to reduce these expenses or increase your income. Doing so will free up money to save, pay off debt, or spend on things that improve your life and make it more enjoyable.

This target goal is somewhat arbitrary, and there may be times when your fixed expenses exceed 50-60% of your take-home pay. For example, if you live in a high-cost area, attend school, or have multiple young children in daycare, your fixed costs may be higher at this time in your life. In this case, do your best to manage other expenses or work to increase your income.

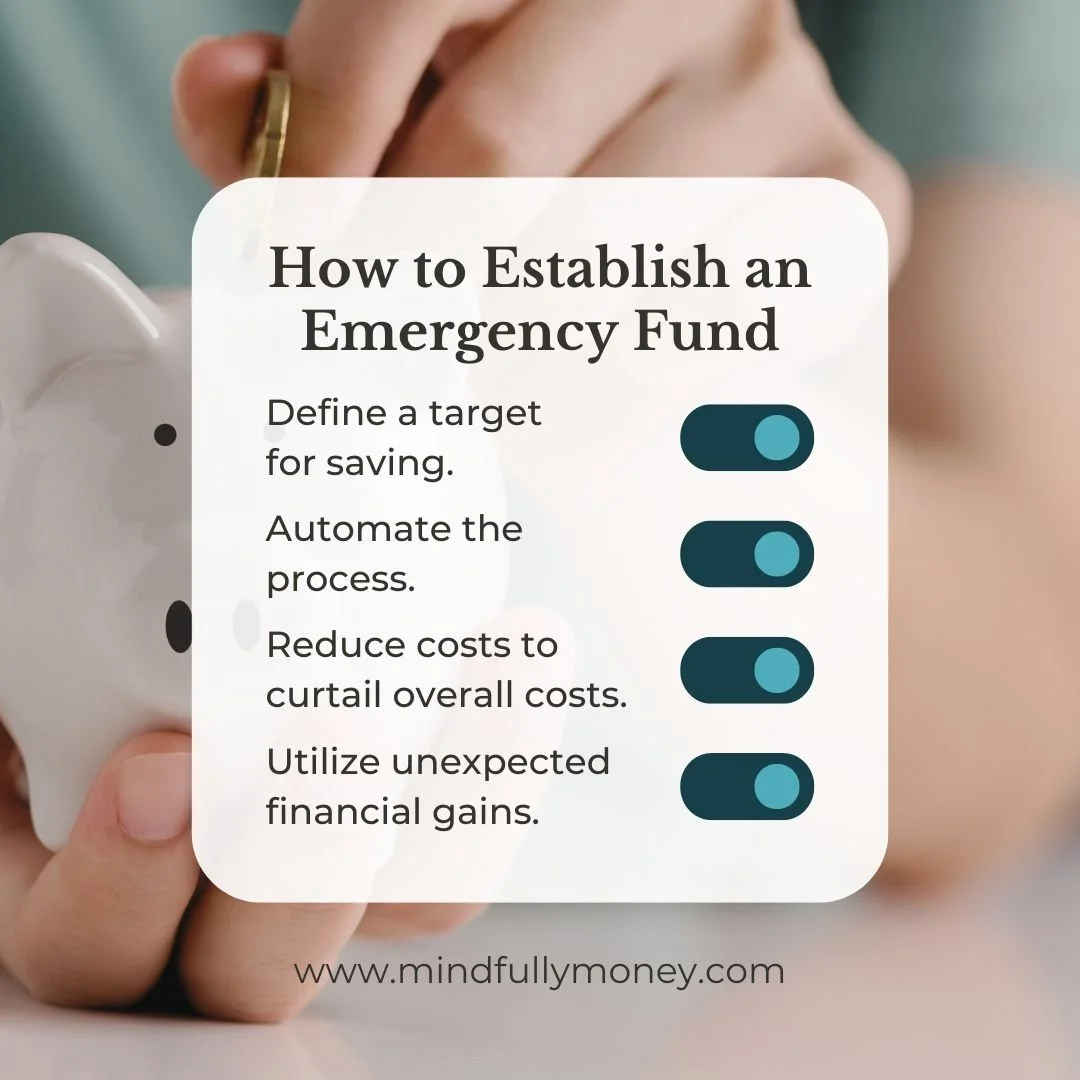

4. Emergency Fund Ratio (Liquidity Ratio)

You’ve probably heard that having an emergency fund is crucial—a savings buffer to cover bills if you lose your job or face unexpected expenses. But how much should you have saved, and how can you measure it?

What is the emergency fund ratio?

The emergency fund or liquidity ratio measures how long you could cover your expenses if you lost your income.

To calculate it, take the total amount you have in accessible savings (excluding retirement or other investments) and divide it by your average monthly expenses. This gives you the number of months you could sustain your current lifestyle without additional income.

For example, if you have $15,000 in savings and your monthly expenses are $5,000, your calculation would be $15,000 ÷ $5,000 = 3. This means you could cover your bills for three months before needing to make significant changes or find new employment.

*You might use the fixed expenses number you calculated earlier to ensure you can cover essential costs. However, for a more conservative approach, include all your monthly expenses in this calculation.

Emergency Fund Ratio Goal:

Aim for 3-6 months of expenses.

This range is commonly recommended, but your target may vary based on your comfort level, job security, the time it might take to find new employment, and other ways you could replace lost income.

While three months is a minimum, having more can provide greater peace of mind. Assess your overall financial situation and consider how you'd feel if you had only three months' worth of savings. Your comfort level will help you decide if you need a larger safety net.

Common Challenges and Tips

Building an emergency fund can be challenging, especially if you’re managing debt or have other financial priorities. Start by setting aside small, manageable amounts each month and gradually increase your contributions. Automating your savings can also help you stay on track.

Impact of Different Scenarios

Your ideal emergency fund amount may vary based on your personal situation. For instance, if you have dependents or work in a volatile industry, you might need more than the standard recommendation. Similarly, if you have a dual-income household with a stable job, you might be comfortable with a lower amount.

By tailoring your emergency fund to your unique circumstances, you can ensure you have a safety net that provides both security and peace of mind.

5. Savings Rate

Your savings rate reflects how much of your income you’re setting aside for future goals, particularly retirement. It can vary depending on whether you're focusing specifically on retirement savings or savings in general. Understanding and optimizing your savings rate is crucial for building a secure financial future.

How to Calculate Your Savings Rate:

To determine your savings rate, first calculate the total amount you save each month. This includes contributions to retirement accounts, college savings, general investments, your emergency fund, and any other long-term financial goals. Then, divide this amount by your total income. The result will be your savings rate.

For instance, if you save $1,000 each month and your monthly income is $5,000, your savings rate is $1,000 ÷ $5,000 = 20%.

Savings Rate Goal

Your ideal savings rate can vary based on your financial situation and goals. Generally, aim for the following:

Overall Savings Rate: 15-20% of your take-home pay. This includes contributions to retirement accounts and savings for other financial goals.

Retirement Savings Rate: 10-15% of your gross income (before taxes and deductions). This should include any employer contributions to retirement plans such as 401(k)s or similar programs.

It’s important to note that these are general guidelines. Your ability to meet these targets will depend on your current financial situation and goals. If saving 15-20% seems challenging right now, start with whatever amount you can manage. Even small contributions can add up over time and help you build the savings habit.

Getting Started

If you're not yet saving, begin by setting aside a modest amount each month and gradually increase it as your financial situation improves. The key is to start building the habit of saving. It’s more beneficial to consistently save a smaller amount than to delay saving entirely until you can contribute a larger sum.

Adjusting Your Savings Rate

As your income grows or your financial goals evolve, revisit and adjust your savings rate. Regularly reviewing your savings plan ensures that you're staying on track to meet your long-term objectives.

By understanding and optimizing your savings rate, you can better prepare for future expenses and work towards achieving your financial goals with confidence.

How to Know if You’re Saving Enough for Retirement

How to Create a Savings Plan that Works for You

6. Housing Ratio

Your housing ratio measures what percentage of your income goes toward housing expenses. This includes rent and renter's insurance for tenants, or mortgage payments, property taxes, and homeowners insurance for those who own their homes.

How to Calculate Your Housing Ratio

To calculate your housing ratio, add up all your monthly housing costs. This total should include:

Rent or mortgage payments

Property taxes

Homeowners or renter’s insurance

Then, divide this total by your gross income (the amount you earn before taxes and other deductions).

For example, if your monthly housing costs are $1,500 and your gross monthly income is $5,000, your housing ratio would be $1,500 ÷ $5,000 = 30%.

Why the Housing Ratio Matters

Your housing ratio is a key indicator of how much of your income is committed to housing expenses. This number helps you gauge whether your housing costs are manageable within your overall budget.

A lower housing ratio typically means you have more flexibility in your budget for other expenses, savings, and discretionary spending. It also reflects a healthier financial balance, allowing you to comfortably cover your bills without stretching your budget too thin.

Lenders often use the housing ratio to assess how much you can afford when applying for a mortgage. While this ratio is a useful guideline for lenders, it’s also a good benchmark for personal financial health.

Housing Ratio Goal: 28% or Lower

Ideally, your housing ratio should be 28% or lower. This means that no more than 28% of your gross income should go toward housing costs. Keeping your housing ratio within this range helps ensure that you maintain financial flexibility and can comfortably meet other financial goals and obligations.

If your housing ratio is above 28%, you may want to evaluate your housing costs and consider ways to reduce them. This might include refinancing your mortgage, exploring more affordable housing options, or increasing your income.

By managing your housing ratio effectively, you can help ensure that your housing expenses fit comfortably within your budget, supporting overall financial stability and well-being.

7. Debt-to-Income Ratio (DTI)

Your debt-to-income ratio (DTI) gives you a snapshot of how much of your income is dedicated to debt payments. It’s a key metric that lenders use to gauge your ability to manage additional debt, but it’s also important for your own financial health and stress management.

What is the Debt to Income Ratio?

To calculate your DTI, combine your total monthly debt payments—including housing costs, credit card payments, student loans, auto loans, and other obligations—and divide this sum by your gross monthly income (your income before taxes and deductions).

For example, if your gross monthly income is $5,000 and your monthly debt payments (including mortgage/rent, car loan, and credit card payments) total $1,500, your DTI would be $1,500 / $5,000 = 0.30, or 30%.

What does your Debt to Income Ratio tell you?

Your DTI provides a clear picture of your debt burden relative to your income. A lower DTI means you have more of your income available for savings and discretionary spending, while a higher DTI indicates that a significant portion of your income is tied up in debt payments, which can limit your financial flexibility.

Debt to Income Ratio Goal: 36% or lower

While 36% is a commonly recommended threshold, specific numbers can vary depending on the lender and type of loan. Maintaining a DTI of 36% or lower helps ensure that your debt payments are manageable and reduces financial stress.

Why the Debt to Income Ratio Matters

A lower DTI indicates that a smaller portion of your income is committed to debt payments, giving you more flexibility to handle unexpected expenses and saving for future goals. Keeping your DTI in check can enhance your financial stability and reduce the likelihood of relying on high-interest debt.

If your DTI is higher than 36%, consider strategies to reduce it, such as paying down existing debt, consolidating high-interest loans, or increasing your income.

Additional Tips

Regularly review your DTI to monitor your progress in managing debt.

If you’re planning to take on new debt, such as a mortgage or car loan, calculate how it will affect your DTI to ensure it remains within a manageable range.

Use your DTI as a tool to set financial goals and track improvements over time.

Understanding and managing your DTI is crucial for maintaining financial health and achieving long-term stability.

8. Credit Score

Your credit score isn't a ratio, but it's an essential financial metric that everyone needs to know. Your credit score can affect your ability to get mortgages and other loans, qualify for rental leases, determine interest rates, insurance premiums, utility costs, and even job opportunities.

What is a Credit Score?

Your credit score measures your creditworthiness to a lender, indicating how likely you are to repay your debts on time. It’s not a measure of how good you are with money, but rather a snapshot of your credit reliability based on your credit history.

A credit score is calculated using different formulas, such as FICO or VantageScore. These scores are derived from information in your credit report, which is maintained by the three main credit bureaus: Experian, Equifax, and TransUnion.

If you need a deeper dive into these terms and how credit works, check out my guide to managing your credit or watch my free credit webinar.

How to Find Your Credit Score

Credit scores are more accessible than ever. Many credit card issuers and banking institutions offer free access to your credit score. If yours doesn't, you can sign up for free services like Credit Karma or create an account with Experian, Equifax, or TransUnion.

Additionally, you should regularly check your credit report through annualcreditreport.com. Regular monitoring can help you catch errors or signs of identity theft early.

Credit Score Goal: 700 or higher

Generally, a credit score above 700 is considered good. The higher your score, the better your chances of qualifying for mortgages, loans, and credit cards at lower interest rates. A high credit score can significantly impact your financial opportunities and costs.

Why Your Credit Score Matters

A good credit score can save you money by qualifying you for lower interest rates on loans and credit cards. It can also make it easier to rent an apartment, get a job, or set up utility services without large deposits. Understanding and improving your credit score is crucial for long-term financial health and stability.

Additional Tips

Pay on Time: Your payment history is one of the most significant factors affecting your credit score. Always aim to pay your bills on time.

Keep Balances Low: Try to keep your credit card balances low relative to your credit limits. High balances can negatively impact your score.

Limit New Credit Applications: Each new credit application can cause a small, temporary drop in your score. Only apply for new credit when necessary.

Check for Errors: Regularly review your credit reports for inaccuracies and dispute any errors you find.

By understanding and managing your credit score, you can improve your financial standing and take advantage of better financial opportunities.

Remember, these numbers and ratios are not here to make you feel bad about your financial situation. They are tools to give you a clearer picture of where you stand and what areas might need attention. Think of them as a roadmap to help you navigate your financial journey.

If your numbers aren’t where you’d like them to be, don’t get discouraged. The goal is to use this information to make informed decisions and set realistic, achievable goals. Small, consistent changes can lead to significant improvements over time.

You have the power to take control of your finances and make choices that align with your goals and values.

Whether you need to adjust your budget, build an emergency fund, or work on your credit score, these numbers are simply a starting point.

If you find this process overwhelming, consider reaching out to a financial coach. They can offer guidance, support, and accountability, helping you create a plan that works for you.

Ultimately, your financial health is about making progress and finding a balance that allows you to live the life you want. Use these ratios as benchmarks, and remember that improving your financial situation is a journey, not a race.

Pin this image to Pinterest to save it for later: